Buyer Beware: China’s Risky Commodity Investments

A few years ago, Western countries feared that China’s forays into Africa would cut them off from commodities. In light of current low prices it looks as if China made a mistake when it secured access to resources through risky investments.

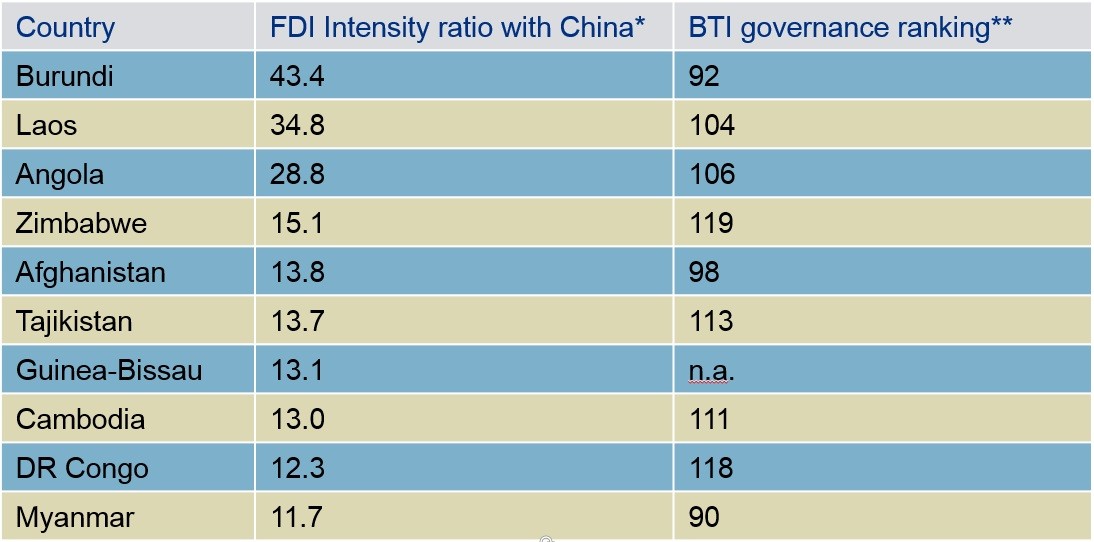

What do countries like Afghanistan, Angola, Burundi, Cambodia, the Democratic Republic of Congo, Guinea Bissau, Laos, Myanmar, South Sudan, Tajikistan and Zimbabwe have in common? They are among the poorest countries in the world and are all ranked as “hard-line autocracies” as well as either “poorly functioning” or “rudimentary” market economies in the Bertelsmann Transformation Index (BTI).

Second, all of them are prime destinations for investors from China. The share these countries have in China’s total foreign direct investment (FDI) by far exceeds their importance for overall global flows of FDI. In other words, these countries are not attractive to foreign investors, except to investors from China.

The reason for China’s interest in investing in some of the poorest regions of Africa and Central Asia is obvious. These countries offer access to natural resources, even if this access is constrained by extremely difficult logistical, economic, social and political conditions. The lack of these fundamentals deters investors from OECD countries who fear controversies about the neglect of social, ecological and political standards.

Trading investment for exclusive access

China has no such qualms. In line with its aim to ensure long-term control over access to commodities, Beijing negotiated forward contracts with the governments of the sourcing markets: China provides and pays for the logistics and infrastructure to extract and deliver the resources. In return it receives exclusive access to them over a longer period of time.

The profitability of these contracts is based on forecasts of future commodity prices relative to the spot price of the infrastructure provided by China. At a time of soaring commodity prices in the years prior to the financial and economic crisis of 2008, the Western world was greatly concerned about China’s aggressive sourcing strategy. China was criticized for its neglect of standards for labor rights, environmental protection and good governance. And many feared that China cut Western competitors off from access to scarce resources.

As it turns out now, such fears may have been unnecessary. China’s deals were based on forecasts, which relied on pre-2008 price movements and pre-2008 assumptions for growth of world demand, including domestic demand in China. Almost ten years later, the world looks entirely different, and it seems that China has become a victim of miscalculation.

Commodity and energy prices have plummeted in a way and at a speed that was not foreseen. The outlook for future demand looks sluggish in particular due to unexpected growth declines in emerging markets and especially in China. It is therefore highly likely that China has earned a much lower profit than expected from its overseas sourcing deals, and that it would have been cheaper to buy these commodities on the spot market without forward contracts and infrastructure investment deals. To make matters worse, political unrest in some of China’s partner countries even puts the fulfillment of these country’s commitments in question, as is currently the case in South Sudan.

* The relative bilateral FDI intensity ratio measures the importance of the host economy in the outward stock of the investor country compared to the importance of the host economy in global FDI flows.

** Ranking among 129 developing and transformation countries in the BTI Management Index.

Exploring the rationale of the Chinese strategy is highly speculative. It was probably based on a combination of economic and geopolitical motivations. Estimates for future demand were based on China’s past high economic growth rates, and precautionary actions were taken for potential future confrontation with Western countries over commodity sourcing.

China’s has to revisit its sourcing model

Regardless of the true motivations, the strategy needs a revision. The economic costs of China’s sourcing model are simply too high. Rather than going it alone, China should share the risks of its investments by entering consortia with other partners, including companies from Western countries. It should also allow private international financial markets to participate in the funding of overseas resource extraction projects. Capital costs for China are higher than before the global financial crisis. State-owned Chinese banks have stockpiled non-performing loans from investment in domestic asset markets, including housing. Adding non-profitable commodity investment abroad to these portfolios would be a grave mistake.

Politically, the “going alone strategy” no longer fits into the framework of new multilateral finance institutions (AIIB, NDC, Silk Road Fund), which were all initiated and powered by China. But if China wants to channel its investments in autocratic and/ or less developed countries through these institutions, it will have to subject them to a screening process to determine whether they comply with ecological and social standards, including those established by the UN Sustainable Development Goals (SDG). Compliance with such standards is crucial to build the credibility of these new institutions and to establish them as trusted borrowers in international financial markets.

This is not to say that China should entirely rely on buying in spot markets to secure its future supply of energy and other resources. Direct investments in commodities have to remain part of the strategy if China’s planners want to prevent the risk of shortages once global demand recovers. But Chinese investors should make future investments through partnerships and consortia and in compliance with international standards. Replacing China’s “going it alone” with a “going together” strategy would benefit all sides involved. It would hopefully lower the environmental and social risks of resource extraction in the host countries, and it would decrease their economic dependency on one single buyer. For China, it would mitigate the financial risks of these investments. Lastly, it would help build confidence in the international community that China is not gearing up for a war over resources.

Rolf J. Langhammer is Senior Fellow at the Kiel Institute for the World Economy and Senior Policy Fellow for China in the Global Economy at the Mercator Institute for China Studies (MERICS). He is member of the BTI Board, an interdisciplinary group of transformation and development experts.

This article was first published on MERICS blog.